Articles

- County May Use Nonjudicial Foreclosure for Nuisance Abatement LiensThe Court of Appeals held in a 2019 case that a County may sell a property in a nonjudicial tax foreclosure sale based upon a nuisance abatement lien. The nuisance abatement statute at O.C.G.A. 41-2-9 provides in part: “It shall be the duty of the appropriate county tax commissioner or municipal tax collector or city …

County May Use Nonjudicial Foreclosure for Nuisance Abatement Liens Read More »

- Judicial Foreclosure Sale Requires Notice of Sale to All Interest HoldersThe Court of Appeals held in a 2019 case that any party with a lien or property interest is entitled to specific notice of the foreclosure sale in addition to the published notice, and in addition to any general notice by being a party to the judicial foreclosure lawsuit. In Georgia Home Appraisers, Inc. v. …

Judicial Foreclosure Sale Requires Notice of Sale to All Interest Holders Read More »

- Determining Priority of Tax Sale Excess Funds in InterpleaderA common question arises regarding which ownership and lien interests will have priority to excess funds from a tax sale. A 2019 decision by the Federal District Court for the Northern District of Georgia waded through a thorny dispute involving competing claims regarding 1) the underlying property owner (and a member of the limited liability …

Determining Priority of Tax Sale Excess Funds in Interpleader Read More »

- Fidelity National Title Tax Sale Underwriting Procedures

While property may generally be considered “marketable” after a tax sale and conventional quiet title, certain insurers may choose to have higher standards. On September 9, 2017, Fidelity National Title Insurance Company issued Bulletin 2017-GA10 with updated underwriting guidelines for insuring properties involved in tax sales. These standards are higher than those listed in the Georgia …

While property may generally be considered “marketable” after a tax sale and conventional quiet title, certain insurers may choose to have higher standards. On September 9, 2017, Fidelity National Title Insurance Company issued Bulletin 2017-GA10 with updated underwriting guidelines for insuring properties involved in tax sales. These standards are higher than those listed in the Georgia …Fidelity National Title Tax Sale Underwriting Procedures Read More »

- Court should not appoint Special Master sua sponte for Conventional Quiet Title

For a conventional quiet title action, only the Plaintiff may request a special master. The holding of the Court of Appeals in the case of Patel v. Patel, 802 S.E.2d 871 (Ga. App. 2017) reversed a trial court for appointing a special master sua sponte: “By the plain language of the statutory authority, when a quiet …

For a conventional quiet title action, only the Plaintiff may request a special master. The holding of the Court of Appeals in the case of Patel v. Patel, 802 S.E.2d 871 (Ga. App. 2017) reversed a trial court for appointing a special master sua sponte: “By the plain language of the statutory authority, when a quiet …Court should not appoint Special Master sua sponte for Conventional Quiet Title Read More »

- Quiet title judgment may be obtained by default after service by publication

When a defendant in a quiet title action is served by publication, their deadline to respond is 60 days after the Order for service, and they are in default if they do not then answer. Once 15 days to open that default has expired, then the plaintiff is entitled to seek a default judgment. In …

When a defendant in a quiet title action is served by publication, their deadline to respond is 60 days after the Order for service, and they are in default if they do not then answer. Once 15 days to open that default has expired, then the plaintiff is entitled to seek a default judgment. In …Quiet title judgment may be obtained by default after service by publication Read More »

- Offer to pay redemption price must be actually made

To redeem a tax deed, the redeeming party much actually tender the redemption price and offer to pay the required sum. It is not enough to claim a “willingness” to pay, or claim that tender was “futile” because the tax deed holder expressed that it believed the redeeming party had no right to redeem and …

To redeem a tax deed, the redeeming party much actually tender the redemption price and offer to pay the required sum. It is not enough to claim a “willingness” to pay, or claim that tender was “futile” because the tax deed holder expressed that it believed the redeeming party had no right to redeem and …Offer to pay redemption price must be actually made Read More »

- Barment notice can contain “variable” deadline to redeem

A typical problem in barring the right to redeem a tax deed is how to set the Deadline. The tax deed holder sets the Deadline in advance when the notice is drafted and sent to be published. But the tax deed holder cannot guarantee that all interested parties will receive the barment notice before the …

A typical problem in barring the right to redeem a tax deed is how to set the Deadline. The tax deed holder sets the Deadline in advance when the notice is drafted and sent to be published. But the tax deed holder cannot guarantee that all interested parties will receive the barment notice before the …Barment notice can contain “variable” deadline to redeem Read More »

- Redeeming creditor of a tax-sale property does not have a priority lien against excess funds arising from that sale

In a highly-anticipated decision, the Georgia Supreme Court created a “bright-line rule” that “a redeeming creditor of a tax-sale property does not have a priority lien against excess funds arising from that sale.” DLT List, LLC v M7Ven Supportive Housing & Development Group, 301 Ga. 131, 800 S.E.2d 362 (2017). This decision overruled a previous line …

In a highly-anticipated decision, the Georgia Supreme Court created a “bright-line rule” that “a redeeming creditor of a tax-sale property does not have a priority lien against excess funds arising from that sale.” DLT List, LLC v M7Ven Supportive Housing & Development Group, 301 Ga. 131, 800 S.E.2d 362 (2017). This decision overruled a previous line … - “Buyer beware” at tax sales

Purchasing a tax deed on the courthouse steps has risks which require a purchaser to conduct due diligence. A 2009 decision by the Georgia Court of Appeals highlights the risk of failing to do so. A tax deed buyer paid $161,000 for 3.64 acres of unimproved land, mistakenly believing it was buying a two-story house. …

Purchasing a tax deed on the courthouse steps has risks which require a purchaser to conduct due diligence. A 2009 decision by the Georgia Court of Appeals highlights the risk of failing to do so. A tax deed buyer paid $161,000 for 3.64 acres of unimproved land, mistakenly believing it was buying a two-story house. … - Get a transcript for Special Master proceedings to preserve appeal

Special master proceedings often occur in a conference room instead of a courtroom, and may seem informal. However, the Court will eventually rely upon findings made by the special master. Therefore, if you want to be able to seek appellate our trial court review of the special master’s factual findings, it is essential to have …

Special master proceedings often occur in a conference room instead of a courtroom, and may seem informal. However, the Court will eventually rely upon findings made by the special master. Therefore, if you want to be able to seek appellate our trial court review of the special master’s factual findings, it is essential to have …Get a transcript for Special Master proceedings to preserve appeal Read More »

- Successive tax lien sales are impermissible

The Georgia Supreme Court has held that once a tax sale has occurred, then it is not permissible for additional tax lien sales to proceed based upon competing tax liens which existed at the time of the sale. DRST Holdings Ltd v AGIO Corporation, 282 Ga 903 (2008). In DRST Holdings, DeKalb County held an …

The Georgia Supreme Court has held that once a tax sale has occurred, then it is not permissible for additional tax lien sales to proceed based upon competing tax liens which existed at the time of the sale. DRST Holdings Ltd v AGIO Corporation, 282 Ga 903 (2008). In DRST Holdings, DeKalb County held an … - Sovereign Immunity applies to Conventional Quiet Title For Now

In the case of TDGA LLC v CBIRA, LLC, 298 Ga. 510, 512 (2016), the Georgia Supreme Court held that “the State and its agencies are immune from suit under OCGA § 23–3–40” which is the conventional quiet title procedure. However, in its next breath, the Court held that “an in rem quiet title action …

In the case of TDGA LLC v CBIRA, LLC, 298 Ga. 510, 512 (2016), the Georgia Supreme Court held that “the State and its agencies are immune from suit under OCGA § 23–3–40” which is the conventional quiet title procedure. However, in its next breath, the Court held that “an in rem quiet title action …Sovereign Immunity applies to Conventional Quiet Title For Now Read More »

- Barment is incomplete without publication and service

When a tax deed purchaser sent a Notice of Right to Redeem to the Defendant in FiFa by certified mail, but did not also publish the notice in the legal organ, the Georgia Supreme Court held that the right to redeem had not been barred. In the case of Reliance Equities LLC v Lanier 5, …

When a tax deed purchaser sent a Notice of Right to Redeem to the Defendant in FiFa by certified mail, but did not also publish the notice in the legal organ, the Georgia Supreme Court held that the right to redeem had not been barred. In the case of Reliance Equities LLC v Lanier 5, …Barment is incomplete without publication and service Read More »

- Void deed of redemption prevents barment until set aside

A novel problem recently faced the Court of Appeals, when it needed to decide whether a tax deed purchaser could conduct a barment, after it had mistakenly recorded a void Quitclaim Deed of Redemption to the Defendant in Fi.Fa. The decision was pragmatic and noted that, if a party did want to redeem in that …

A novel problem recently faced the Court of Appeals, when it needed to decide whether a tax deed purchaser could conduct a barment, after it had mistakenly recorded a void Quitclaim Deed of Redemption to the Defendant in Fi.Fa. The decision was pragmatic and noted that, if a party did want to redeem in that …Void deed of redemption prevents barment until set aside Read More »

- Tax Deed Buyers Owe Homeowners Assessments and Taxes

When a tax deed is purchased, the title is ‘defeasible’ and the purchaser does not have an immediate right of possession. Nevertheless, the Court of Appeals has held that the interest held, even during the redemption period, “is sufficient to render him liable for taxes accruing upon the property [and] . . . this interest …

When a tax deed is purchased, the title is ‘defeasible’ and the purchaser does not have an immediate right of possession. Nevertheless, the Court of Appeals has held that the interest held, even during the redemption period, “is sufficient to render him liable for taxes accruing upon the property [and] . . . this interest …Tax Deed Buyers Owe Homeowners Assessments and Taxes Read More »

- Who can claim excess funds from a tax sale?

Sometimes, the sales price at a tax sale exceeds the amount necessary to satisfy the tax lien. O.C.G.A. 48-4-5(a) explains the process to distribute those excess funds. Generally, excess funds are distributed to owners or lienholders in order of their priority of interest in the property. “Under Georgia law, a tax commissioner holds any excess …

Sometimes, the sales price at a tax sale exceeds the amount necessary to satisfy the tax lien. O.C.G.A. 48-4-5(a) explains the process to distribute those excess funds. Generally, excess funds are distributed to owners or lienholders in order of their priority of interest in the property. “Under Georgia law, a tax commissioner holds any excess … - A Quia Timet Plaintiff must show either record title or prescriptive title

In a Georgia action for Quia Timet Against All the World, the petitioner must be able to show either that they have current record title, or that they have current prescriptive title. But a mere expectancy is not enough. In the case of Rivermist Homeowners Ass’n, Inc., In re, 244 Ga. 515, 260 S.E.2d 897 (1979), …

In a Georgia action for Quia Timet Against All the World, the petitioner must be able to show either that they have current record title, or that they have current prescriptive title. But a mere expectancy is not enough. In the case of Rivermist Homeowners Ass’n, Inc., In re, 244 Ga. 515, 260 S.E.2d 897 (1979), …A Quia Timet Plaintiff must show either record title or prescriptive title Read More »

- Can Quiet Title be used to remove an easement?

Yes. Quiet Title be used to remove an easement. In the case of Wiggins v. Southern Bell Tel. and Tel. Co., 245 Ga. 526, 266 S.E.2d 148 (1980) the Georgia Supreme Court considered challenges to two easements in the context of a quiet title action. Although the court found the easements to be valid, the case …

Yes. Quiet Title be used to remove an easement. In the case of Wiggins v. Southern Bell Tel. and Tel. Co., 245 Ga. 526, 266 S.E.2d 148 (1980) the Georgia Supreme Court considered challenges to two easements in the context of a quiet title action. Although the court found the easements to be valid, the case … - Do I need possession of the property to seek to quiet title?

Possession of the property must generally shown for a Georgia action for conventional quia timet (with exceptions), but possession does not need to be shown for quia timet against all the world in Georgia. For a traditional conventional quia timet action in equity, the plaintiff had to show that he was in possession of the property. O.C.G.A. § 23-3-42. In …

Possession of the property must generally shown for a Georgia action for conventional quia timet (with exceptions), but possession does not need to be shown for quia timet against all the world in Georgia. For a traditional conventional quia timet action in equity, the plaintiff had to show that he was in possession of the property. O.C.G.A. § 23-3-42. In …Do I need possession of the property to seek to quiet title? Read More »

- Who should pay the special master in a quiet title action?

The special master procedure used in a conventional quiet title action is the same as is used in an action to quiet title against all the world. O.C.G.A. 23-3-43. It is up to the Court to set “reasonable compensation” for the special master, and those “fees are to be taxed in the discretion of the …

The special master procedure used in a conventional quiet title action is the same as is used in an action to quiet title against all the world. O.C.G.A. 23-3-43. It is up to the Court to set “reasonable compensation” for the special master, and those “fees are to be taxed in the discretion of the …Who should pay the special master in a quiet title action? Read More »

- Do I get a jury trial in a quiet title action?

Whether or not you get a jury trial in a quiet title action depends upon the type of quiet title action. In a conventional quiet title action, the Georgia Supreme Court has held that there is no right to a jury trial. See Davis v. Harpagon Co., LLC, 637 S.E.2d 1, 281 Ga. 250 (2006) (“Davis contends …

Whether or not you get a jury trial in a quiet title action depends upon the type of quiet title action. In a conventional quiet title action, the Georgia Supreme Court has held that there is no right to a jury trial. See Davis v. Harpagon Co., LLC, 637 S.E.2d 1, 281 Ga. 250 (2006) (“Davis contends … - Quiet title can be used to set aside a forged deed

If you own property, and someone forges a deed which purports to convey your interest in the property, what should you do? In 2010, the Georgia Supreme Court, in the case of Brock v. Yale Mortg. Corp., 287 Ga. 849, 700 S.E.2d 583 (2010), confirmed that a conventional quiet title action can be used to cancel …

If you own property, and someone forges a deed which purports to convey your interest in the property, what should you do? In 2010, the Georgia Supreme Court, in the case of Brock v. Yale Mortg. Corp., 287 Ga. 849, 700 S.E.2d 583 (2010), confirmed that a conventional quiet title action can be used to cancel …Quiet title can be used to set aside a forged deed Read More »

- Do Georgia tax deeds ripen by prescription?

A tax deed can ripen by prescription, but the statute isn’t exactly what it seems. O.C.G.A. 48-4-48(b) provides that title under a tax deed executed after July 1, 1996 ripens 4 years after the tax deed is recorded in the land records. Disability exception. But O.C.G.A. 48-4-48(c) has an exception. If the prior owner (i.e. the Defendant …

A tax deed can ripen by prescription, but the statute isn’t exactly what it seems. O.C.G.A. 48-4-48(b) provides that title under a tax deed executed after July 1, 1996 ripens 4 years after the tax deed is recorded in the land records. Disability exception. But O.C.G.A. 48-4-48(c) has an exception. If the prior owner (i.e. the Defendant … - How do you quiet title to an IRS Notice of Federal Tax Lien?

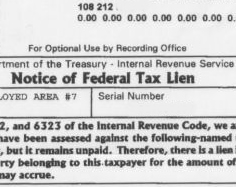

Often, when trying to quiet title to Georgia property, you will encounter an IRS Notice of Federal Tax Lien. Determining how to serve the Internal Revenue Service (IRS) with a quiet title action can be difficult if you don’t know where to look. If your quiet title action is filed in federal court, then follow Federal …

Often, when trying to quiet title to Georgia property, you will encounter an IRS Notice of Federal Tax Lien. Determining how to serve the Internal Revenue Service (IRS) with a quiet title action can be difficult if you don’t know where to look. If your quiet title action is filed in federal court, then follow Federal …How do you quiet title to an IRS Notice of Federal Tax Lien? Read More »